On a value spectrum, billions spent on cities' transit systems will probably deliver more benefit than billions spent on VIA.

In the past, when this even came up in discussion at a political level in Alberta, that is exactly what they said. Build out the LRTs before worrying about rail.

IMO, it's a bit of a short sighted opinion. Intercity rail serves a different purpose and it's network effects would have wider, longer term benefits.

My biggest criticism is that their desire to get shovels in the ground (understandable), may have led to them not considering or pitching opportunity investments.

From what I've read so far, the rough breakdown is this: $0.9B for the fleet, $0.1B for Ottawa-Montreal, $1B for Montreal-Quebec and $2B for Toronto-Peterborough-Ottawa.

What we don't know is what $1-2B more would yield. Would an extra billion twin track the whole corridor allowing for substantially more frequencies? Would a billion on Ottawa-Montreal allow that route to get closer to HSR speeds? How much capability does an extra billion on Toronto-Peterborough-Ottawa yield? How much travel time is cut and how much would ridership get boosted?

I'm a little conflicted on VIA being more transparent. Would more information be nice? Absolutely. But we've all seen past projects get canned as opposition takes advantage of unrefined estimates to argue incessantly. It is after all, way easier to argue against building something than for building something. And the modern history of this country is one of skeptics helping to perpetuate inaction and mediocrity.

Nope. A network can have trains from more than one operator. That said, I kinda wish VIA would takeover the route to art least North Bay. But that's between the feds and Queen's Park to figure out.

If they were to take it over, they could buy the CN line between Washago and North Bay. I doubt it will ever happen.

Quote:

Originally Posted by Truenorth00

Indeed. Hopefully, the boost from HFR can get them going beyond daily. Even if it's not the entire route.

What parts of those routes would be far enough that more than daily would work? I feel that it would make the most sense to add the whole route. Take Moncton to Halifax. If the whole line of Ocean was 2x a day, that part would be the busier part.

Quote:

Originally Posted by Truenorth00

The lift from HFR won't be substantial. You might take a 10 hr train ride more often, with improved service, better connections, etc. But demand for a multi-day journey isn't likely to change much.

I'll be that running the Canadian daily would improve ridership on it throughout the route. If the section between Toronto and Capreol could be done in a reasonable time compared to driving, more people between there would switch over. Maybe the overnight journeys won't see an increase, but anything within a reasonable distance to the big cities along it likely would.

My biggest criticism is that their desire to get shovels in the ground (understandable), may have led to them not considering or pitching opportunity investments.

From what I've read so far, the rough breakdown is this: $0.9B for the fleet, $0.1B for Ottawa-Montreal, $1B for Montreal-Quebec and $2B for Toronto-Peterborough-Ottawa.

What we don't know is what $1-2B more would yield. Would an extra billion twin track the whole corridor allowing for substantially more frequencies? Would a billion on Ottawa-Montreal allow that route to get closer to HSR speeds? How much capability does an extra billion on Toronto-Peterborough-Ottawa yield? How much travel time is cut and how much would ridership get boosted?

I'm a little conflicted on VIA being more transparent. Would more information be nice? Absolutely. But we've all seen past projects get canned as opposition takes advantage of unrefined estimates to argue incessantly. It is after all, way easier to argue against building something than for building something. And the modern history of this country is one of skeptics helping to perpetuate inaction and mediocrity.

They likely want to straighten it out before double tracking it.

In the past, when this even came up in discussion at a political level in Alberta, that is exactly what they said. Build out the LRTs before worrying about rail.

IMO, it's a bit of a short sighted opinion. Intercity rail serves a different purpose and it's network effects would have wider, longer term benefits.

Also, this analysis holds way less value in the era of climate change. Flying is disproportionately damaging. And so is going to get disproportionately expensive. As will long drives in an F150. As carbon taxes go up, intercity rail infrastructure becomes far more important economically. Especially on city pairs with a large number of flights.

Skepticism is not neutrality. Via has promised a system with unusually low per km costs, an unusually high average speed as a percentage of max speed, an unusually high ridership increase projection for a relatively small increase in speed, and implied that it will be profitable so that investors will pay for a significant portion (a rarity in the passenger rail business).

On top of this Via has released little of its background work/analysis, has not actually released a detailed route map and doesn’t seem to have spent much on geotechnical studies, design, business modelling, etc.

Maybe Via has invented the equivalent of railway Moneyball and has figured out a totally new business model unused elsewhere, but they have not given us any reason to believe that.

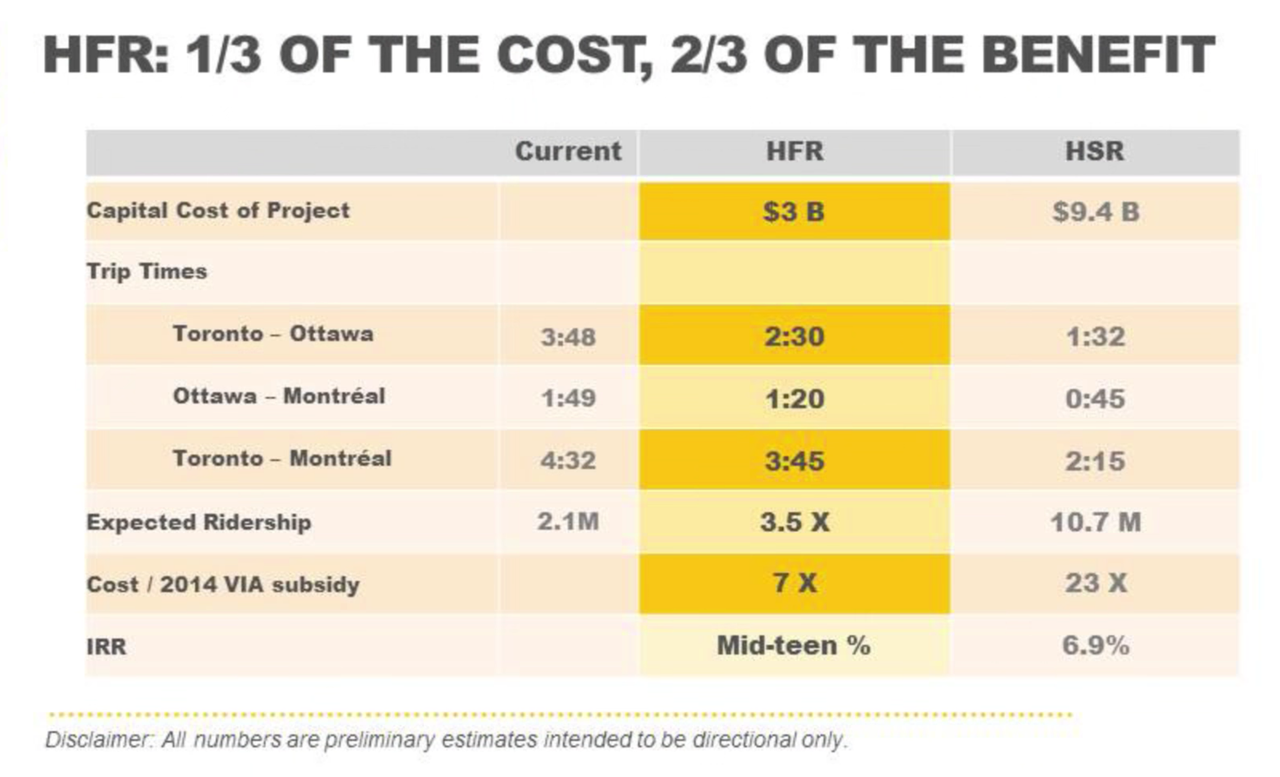

VIA has not claimed that HFR would be profitable. They clearly acknowledge that it will, like most forms of public transportation in the West, require significant operating subsidies. Any investor profit will be based on a PPP whose terms ensure the private partner receives an investment return based on the public sector providing sufficient funding. Here's a screen grab from one of their promotional videos where the CEO gives a presentation on the proposal. It clearly shows, as the CEO states, that the subsidy with HFR is expected to be 7x higher than 2014 corridor average but much lower than with HSR. In other words, not a new business model that magically makes public transport profitable, just a way to improve the service without the much higher cost of HSR.

That being said, skepticism is indeed neutrality - not as a final conclusion, but as an intermediate state awaiting more information. It is the act of not accepting a claim as true until more information is provided. If someone feels they already have enough information to draw an opposing conclusion before seeing the information behind an assertion, that isn't skepticism; it's disagreement or opposition. Obviously there's nothing wrong disagreement is wrong as a general principle. I just feel skepticism is appropriate in this instance. You're welcome to disagree of course but that's my position.

__________________

"The reasonable man adapts himself to the world; the unreasonable one persists in trying to adapt the world to himself. Therefore all progress depends on the unreasonable man." - George Bernard Shaw Don't ask people not to debate a topic. Just stop making debatable assertions. Problem solved.

It clearly shows, as the CEO states, that the subsidy with HFR is expected to be 7x higher than 2014 corridor average but much lower than with HSR. In other words, not a new business model that magically makes public transport profitable, just a way to improve the service without the much higher cost of HSR.

I believe you've misinterpreted this graphic.

VIA Rails 2014 subsidy was $398.9M ($317.1M operating + 80.9M capital). $3B / $398.9M is roughly 7 and $9.4B / $398.9M is roughly 23. So, the capital investment for VIA HFR is roughly equivalent to 7x the operating subsidy at that time.

They are not expecting the subsidy for corridor operations to increase with HFR.

That being said, skepticism is indeed neutrality - not as a final conclusion, but as an intermediate state awaiting more information.

"Skepticism"

More like bad faith "I'm just asking questions." nonsense.

And like I said. Nothing gets built in this country, because there's always some "skeptic" to bitch and moan and pick apart every detail until the idea is finally derailed. This one is caught between those want perfection (HSR) and those who don't want to lose their airline status when their employers inevitably tell them to take the newly improved train service.

VIA Rails 2014 subsidy was $398.9M ($317.1M operating + 80.9M capital). $3B / $398.9M is roughly 7 and $9.4B / 398.9M is roughly 23. So, the capital investment for VIA HFR is roughly equivalent to 7x the operating subsidy at that time.

They are not expecting the subsidy for corridor operations to increase with HFR.

Your interpretation is how I interpreted it.

I can't remember if VIA actually said HFR would be profitable or if that was just a discussion point on this forum. Either way, I would say it's likely that the subsidy for HFR will increase as an absolute value, but the number of passengers will increase more thus making the per rider subsidy less. Just because something is subsidized doesn't mean it isn't a good investment - currently all car trips on non toll roads are 100% subsidized.

VIA Rails 2014 subsidy was $398.9M ($317.1M operating + 80.9M capital). $3B / $398.9M is roughly 7 and $9.4B / $398.9M is roughly 23. So, the capital investment for VIA HFR is roughly equivalent to 7x the operating subsidy at that time.

They are not expecting the subsidy for corridor operations to increase with HFR.

Correct. And in subsequent interviews, I believe he suggested that HFR would basically be operationally profitable, negating the need for a subsidy on Corridor East. The rest of VIA would still need subsidies.

This is important because of how many pax Corridor East moves. That's a lot of subsidy in aggregate, regardless of the per pax amount. In 2019, Corridor East required $114M in subsidies.

Would it not make sense to turn Via into our version of the UK's National Rail so VIA can manage the network and build the infrastructure but let private firms bid on operating the trains, etc.?

Would it not make sense to turn Via into our version of the UK's National Rail so VIA can manage the network and build the infrastructure but let private firms bid on operating the trains, etc.?

Maybe, but it's never, ever going to happen so there isn't much value in discussing it. At least for the CN/CP owned stuff.

Where there are lines owned by VIA/GO there may be the potential for a regulator, but it should be a new body, separate from the existing operators. I don't know if it really would provide much value right now though, as the extent that passenger operators conflict with each other is minimal and where it does exist they are probably less dickish than CP and CN at resolving issues.

VIA Rails 2014 subsidy was $398.9M ($317.1M operating + 80.9M capital). $3B / $398.9M is roughly 7 and $9.4B / $398.9M is roughly 23. So, the capital investment for VIA HFR is roughly equivalent to 7x the operating subsidy at that time.

They are not expecting the subsidy for corridor operations to increase with HFR.

Quote:

Originally Posted by Truenorth00

Correct. And in subsequent interviews, I believe he suggested that HFR would basically be operationally profitable, negating the need for a subsidy on Corridor East. The rest of VIA would still need subsidies.

This is important because of how many pax Corridor East moves. That's a lot of subsidy in aggregate, regardless of the per pax amount. In 2019, Corridor East required $114M in subsidies.

I re-watched the presentation and it does seem that he's included the capital cost with subsides which is not typical when discussing public transportation, but in this case it was because he was laying out out the case for a PPP. With a standard PPP model where the private sector pays the upfront capital costs and the government pays a set amount per rider to allow them to make back the investment, that would indeed cause the subsidy to be higher. I'm still not sure I see anything magical about it as that wouldn't be much different than the Canada Line, REM, etc., but it is bit confusing seeing as the proposal has evolved a few times since originally presented and we could definitely use more detail.

__________________

"The reasonable man adapts himself to the world; the unreasonable one persists in trying to adapt the world to himself. Therefore all progress depends on the unreasonable man." - George Bernard Shaw Don't ask people not to debate a topic. Just stop making debatable assertions. Problem solved.

If the travel times drop from 25% to 40% on every route then the public's perception will change for the better. Conversely, if all it does is offer more trains with just better reliability but no meaningful decrease in travel times then any potential further government money for improved rail service will be seen as nothing more than throwing good money after bad.

Just a quick comparison with Germany, which has a per-capita rail ridership which is almost 10 times that of Canada (1,185 km vs. 122 km in 2018):

It’s not that much the average speed which sets Canada (refer to the black lines) and Germany (refer to all other lines) apart…

Using the gravity model of ridership, 7 million riders is a pretty reasonable estimate. Also not unfathomable given existing demand for services. Pre-Covid was doing a decent job filling every new train they added. And that's with current travel times, prices and schedules. HFR will boost frequencies, get travel times down (how much is debatable), and could help get prices down (higher asset utilization should engender some savings). Add in population growth in the major metros and the traffic that goes with that, and it's really not hard to imagine 7 million by 2030. Especially as the intercity commuter market grows as well. And that is a major source of business for most major rail lines in other countries.

Quote:

Originally Posted by Truenorth00

There's a mathematician and railnerd who does a good job of explaining how network effects can boost ridership on connecting lines. He does it in the context of high speed rail. But the models with for regular speed rail. Just need different constants.

If you extrapolate from VIA’s 2019 demand figures in the Toronto-Ottawa-Montreal triangle, population growth alone would demand from 3.6 million in 2019 to 4.1 million in 2030. If you add the decrease in generalized travel time (from higher frequencies and shorter travel times), you would already be at 5.5 million:

Skepticism is not neutrality. Via has promised a system with unusually low per km costs, an unusually high average speed as a percentage of max speed, an unusually high ridership increase projection for a relatively small increase in speed, and implied that it will be profitable so that investors will pay for a significant portion (a rarity in the passenger rail business).

On top of this Via has released little of its background work/analysis, has not actually released a detailed route map and doesn’t seem to have spent much on geotechnical studies, design, business modelling, etc.

Maybe Via has invented the equivalent of railway Moneyball and has figured out a totally new business model unused elsewhere, but they have not given us any reason to believe that.

You, ssiguy and swimmer_spe really share the crown for the most boring trolls in this thread, as no amount of debunking your unsubstantiated claims receive, you still don’t miss any occasion to vomit them over us for the one-hundredth time.

Via has promised a system with unusually low per km costs

The per-km costs vary widely by what infrastructure or ROW is already present and what amount of re-alignments and expensive engineering work (bridges, stations or tunnels) is required to achieve the desired service characteristics. If you compare the per-km estimates with HSR in Europe (or the new LRT in Ottawa), they will appear very low, if you compare it with the cost of creating the initial “O-Train” in Ottawa, they might appear high.

an unusually high average speed as a percentage of max speed

Let me just dump again my response from when you made the same incorrect claim three months ago, in the vain hope that you might have somehow developed the intellectual capacity in the meanwhile to process the information I provided you:

Quote:

Originally Posted by Urban_Sky

Quote:

Originally Posted by acottawa

An average speed of 62% of max speed is on the high side. On the track it already owns Via currently operates at 50% of max speed, which is about what the Acela operates at.

There are only three Corridor segments which VIA owns:

In the case of Coteau-Ottawa, the fastest travel time between these two stations translates currently to 70% of the top speed, which is down from 77% in 2005, but still above the 66% HFR aims for between Montreal and Ottawa.

In the case of Ottawa-Brockville, the fastest travel time between these two stations translates currently to 57% of the top speed, which is down from 62% in 1987. Admitedly, HFR aims at 70% between Ottawa and Toronto, but that's only marginally higher than where VIA stands currently (68%) and actually lower than where it stood in 2014 (74%).

Finally, there is Chatham-Windsor, which has basically the same percentages as Ottawa-Brockville.

In short, the ratio between targeted average speed and maximum speed is in line with what has been already achieved in the past and present on the Corridor:

Again, not a technical problem but probably a cost one.

It really speaks volumes about your level of expertise on the subject that even after all the years we've been arguing here, you still don't grasp the difference between High Speed Rail on one hand and conventional intercity rail like HFR on the other.

I'll try to explain this to you without sounding like I'm explaining it to someone who has just joined the discussion, but the more you increase the design speed, the smaller will be the proportion of total distance covered which can actually be upgraded to that speed (because beyond a certain speed, you can no longer have level crossings, share tracks with freight, use legacy signaling systems or fit the minimum radii you require in-between existing buildings and infrastructure). Furthermore, the higher speeds you reach, the more distance you need to cover for a given speed increment. Add to that the fact that you will rarely be able in Europe to link two mass population centers 400 km apart with hitting only one population center of 100k+ and that every stop means that you have to accelerate again from zero, and you might finally start to understand why the percentage of average vs. maximum speed is so low for many HSR systems in Europe - and why it has so little relevance for conventional intercity rail proposals in Canada. Because whatever HFR tries to achieve has already been done before - in Europe and even in Canada:

an unusually high ridership increase projection for a relatively small increase in speed

Similar to what I have shown further above regarding the Toronto-Ottawa-Montreal triangle, that population growth, increased service frequency and reduced travel time alone suggest that passenger figures would increase overall Corridor demand from 4.8 million passengers in 2019 to 6.9 million by 2030. Add to that the positive effects of higher on-time performance and overall service reliability, a better fleet and more seating capacity (the lack of which artificially constraints actual ridership by artificially high ticket prices to price out excess demand on trains without sufficient seating capacity) and a timetable which is no longer forced to neglect the needs of the intermediary markets (like Kingston-Cobourg) in order to minimize travel time on the primary markets (like Toronto-Ottawa) and you might get very close to whatever ridership projections you were referring to:

and implied that it will be profitable so that investors will pay for a significant portion (a rarity in the passenger rail business).

Depending on what proportion of the capital cost is to be financed by the investor, what volume of trains will operate and what amount every train movement will be charged by the investor, any piece of rail infrastructure could be profitable for an investor. Whether that saves the taxpayer money in the long-term (compared to having the project entirely funded by the taxpayer at its historically low borrowing costs) is of course a different story…

***

Quote:

Originally Posted by Truenorth00

I'm a little conflicted on VIA being more transparent. Would more information be nice? Absolutely. But we've all seen past projects get canned as opposition takes advantage of unrefined estimates to argue incessantly. It is after all, way easier to argue against building something than for building something. And the modern history of this country is one of skeptics helping to perpetuate inaction and mediocrity.

The thing is that none of the questions which are likely to arouse NIMBY protests (does the HFR route traverse through community X or will it bypass it and will it have a station or not?) actually matter to VIA’s overarching objective of achieving a travel time of X:XX hours between Y and Z. Therefore, discussing and deciding these questions (i.e. the “How”) before the overall fate of HFR (i.e. the “If”) is decided, will only help those who want to prevent the project…

***

Quote:

Originally Posted by Nouvellecosse

VIA has not claimed that HFR would be profitable. They clearly acknowledge that it will, like most forms of public transportation in the West, require significant operating subsidies. Any investor profit will be based on a PPP whose terms ensure the private partner receives an investment return based on the public sector providing sufficient funding. Here's a screen grab from one of their promotional videos where the CEO gives a presentation on the proposal. It clearly shows, as the CEO states, that the subsidy with HFR is expected to be 7x higher than 2014 corridor average but much lower than with HSR. In other words, not a new business model that magically makes public transport profitable, just a way to improve the service without the much higher cost of HSR.

I’m not sure you are reading that chart correctly: VIA’s overall subsidy need (i.e. operating and capital funding combined) was $398 million in 2014 (i.e. the year in which HFR was first presented to the public). Therefore, a total capital cost of $3 billion for HFR would be 7.5 times what the federal taxpayer spent on VIA in 2014, whereas a total capital cost of $9.4 billion for HSR would be 23.6 times VIA’s cost to the taxpayer in the same year.

In terms of what HFR would do to VIA’s overall subsidy need, I have conducted a back-of-the-envelope business case calculation on Urban Toronto, which suggested that HFR might break even for the federal taxpayer after 33 years:

Quote:

To highlight this, let me conduct this back-of-the-envelope business case.

Let's assume that HFR will double VIA's corridor ridership (i.e. from 4.5 in 2018 to 9.0 million soon after HFR is operational) and increase its scheduled train-mileage by 50% from 8.7 million miles in 2018 to 13.1 million miles per year. Let's also assume that variable revenues are proportional to the ridership and that variable expenses are proportional to variable revenues train-miles. Finally, let's assume that HFR costs $6 billion (as the highest figure I recall seeing anywhere) in capital cost and that operation starts 3 years after the capital cost is paid and that the first 40 years of operation are included for the calculation of the internal rate of return:

Variable revenues in 2018: $294 million

Variable costs in 2018: $217 million

Contribution in 2018: $77 million

Variable revenues per year with HFR: $294 million * 200% = $588 million

Variable costs per year with HFR: $217 million * 150% = $325.5 million

Contribution per year with HFR: $588 million - $325.5 million = $262.5 million

Subsidy saved per year: $262.5 million - $77 million = $185.5 million

Payback-period: $6 billion / $185.5 million => after 33 years of operation

Internal rate of return: 1.1%

I would consider above assumptions as rather conservative (no increase in average fare was assumed, even though a reduction in travel time and increase in frequency and service reliability might increase the willingness to pay, while these three factors might also reduce costs per train-mile), but an IRR of 1.1% is exactly the kind of return which is unattractive for institutional investors, but might still be attractive for a government which can currently borrow for 10 years at approximately 0.6% (thus just over half the IRR I calculated) and which gains from the project in ways which an institutional investor could never participate (e.g. economic stimulation which generates additional tax revenues or environmental benefits which reduce healthcare costs).

***

And now I'm handing over the stage again to our trolls acottawa, ssiguy and swimmer_spe and their ever-same re-posts of the same long-debunked misconceptions and falsehoods, namely that there is hardly any precedent anywhere in the world for what HFR aims to achieve (acottawa), that VIA needs to abandon all its existing operations to pursue HSR instead (ssiguy) or that there is any economic case for restoring at-least-daily passenger rail service between Toronto, Sudbury or Winnipeg (swimmer_spe)...

Last edited by Urban_Sky; Feb 24, 2021 at 6:41 PM.

Reason: Fixing formatting/presentation issues and minor corrections

I'm afraid that (given the amount of trolling in this thread) I have no intention to become a regular again, but I just wanted to remind the readers here that most of the "arguments" exchanged here recently have already been debunked over and over again...

I'm afraid that (given the amount of trolling in this thread) I have no intention to become a regular again, but I just wanted to remind the readers here that most of the "arguments" exchanged here recently have already been debunked over and over again...

No worries, I see you have your hands full over at Urban Toronto.

When it comes to HFR, the only thing that can really change the conversation is news from VIA or the government. Without that all the talk is fairly fruitless.

Like I said, in my experience all those who are whining about HFR are people who don't actually use the train regularly. That includes many of the "skeptics" in this thread. From the Vancouver resident who thinks anything less than HSR is useless based on his vast experience with the Corridor, to the Sudbury resident who thinks that no further investment for inter-metro service is needed at all, to the Ottawa public servant who puts down the project because he knows that his frequent flyer status might be in jeopardy if he's forced to take the train more often. Lots of motivation to be "skeptical" on the project from folks who don't actually travel by train on the proposed route, but not a lot of facts or logic.

But if you actually use Corridor service? HFR looks like an absolute no-brainer. If they announced a 50% increase in project cost, I still wouldn't blink. It is way past time we had decent service between our larger metros. Corridor first. And CalEd next. We need to get on with actually building things in our country.

When it comes to HFR, the only thing that can really change the conversation is news from VIA or the government. Without that all the talk is fairly fruitless.

I look forward to a complete rehash of all the bad faith arguments and non-sequiturs when the government officially launches HFR in the budget.

My concern isn't that you doubted the projection, but rather than you seem (or at least seemed) to reject it. I did notice that your reasoning didn't seem to consider the comparison that I raised, and my intention was to point out that perhaps it should. It shows that there are examples of conventional speed services attracting (greater than) that level of ridership despite the claims from some that it's impossible since only full HSR can compete effectively with airlines. The UK may have 5 times the population of Canada's corridor but we can compare the WCML specifically. While the UK is served by multiple frequent mainline rail corridors (East and West Coast Mainlines, Great Western Mainline, Midland Mainline, et al) the WCML being the most important mainline connecting major metro areas containing about 30 million (but is not the only route connecting most of them). That make the WCML a corridor of about 2.3x the population. So an equivalent percapita ridership would be about 16 million (37/2.3). The UK has ~31% lower auto ownership rates, but also much cheaper flights. Even if we ignore the air aspect and grant that Canada would have 31% lower rail usage percapita due to automobile prevalence, the 16 million would drop to 11 million. Sure the WCML has had frequent service for longer so would have more time to build up patronage and shape travel patterns, so we can drop the ridership by another third. But even after lowering the projected ridership to adjust for all those factors, the resulting number is still so implausibly high that it warrants a "fat chance?"

Fact is, Canada may be a laggard in terms of offering public transportation services, but when reasonable services are offered, we don't fall behind in terms of using them.

I think that skepticism is great, but skepticism represents neutrality, ie you don't know whether or not to believe an assertion until you receive more evidence. It responds to the assertion of "A equals B" with "how do you know?" However, the response of "no it doesn't" is not skepticism, but rather it's own counter assertion. I think it would be great to see the details in the VIA ridership projections, but until then I think true skepticism (neutrality) is warranted. I don't wish to say that the projected number is accurate or inaccurate, but rather that it isn't implausible and therefore doesn't warrant rejection.

I concede that I may have gone a bit far with the "fat chance" comment, but, as I've stated, there are a lot of red flags that make me question the "3x" and "7M" figures.

Your point about Canada's good use of public transportation infrastructure is true. Our issue is certainly more about the lack of infrastructure than our willingness to use it. You also draw some fair comparisons to both the WCML and ECML, and the cheaper air fares as well. No major criticisms there. However, I do have to point out one key difference you didn't mention, and that's that the ECML and WCML connect to a massive rail network that doesn't only have numerous high quality, high speed and high frequency connections to the the whole country, but all of western Europe. That alone would make a huge difference in the ridership potential of the service. It'll be interesting to see how Brexit impacts that ridership.

If we follow the HFR project with improved connections to other markets in the corridor (e.g., Quebec City, London, Windsor), as well as potential connections to US markets, the ridership potential would be far greater. But we are a long way from that, unfortunately.

I don't really want to get into the semantics of "skepticism", as that may start a whole other debate, so I'll say this: I can't outright reject the numbers without seeing the methodology, but given the available information, there are a few aspects that don't fully add up, which I've previously stated. Of course there may be factors I've not considered, but my impression is that the 3x and 7M figures were tied to the initial purported run time of 2.5hrs for Tor-Ott. I don't think it's a coincidence that they seem to have dropped that ridership figure since they've revised the run-time to about 3.25-3.5hrs.

Prev

Prev

Linear Mode

Linear Mode