Quote:

Originally Posted by rivernorthlurker

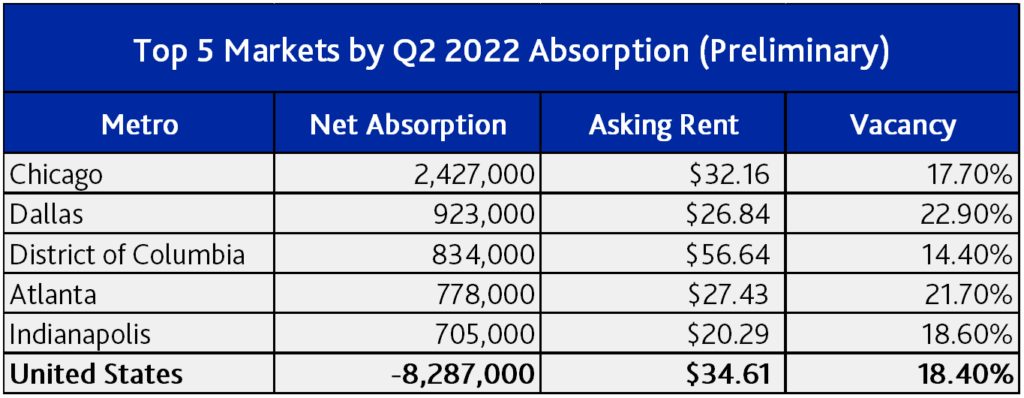

I would love to see the breakdown since there have been some massive high profile 'absorption' during this time like BMO tower, 110 Wacker, and possibly Salesforce. I'mm not sure how/when they count these.

It would be more exciting if the high numbers weren't coming from single massive projects.

Does anyone know what 'completions' are in this context?

|

I went through some figures for the downtown area from the Cushman and Wakefield reports. I think some of the data is categorized differently in the Moody’s article and table, but overall the big picture seems the same.

Basically, 110 N Wacker and Fulton Market were the big additional inventory bombs this year

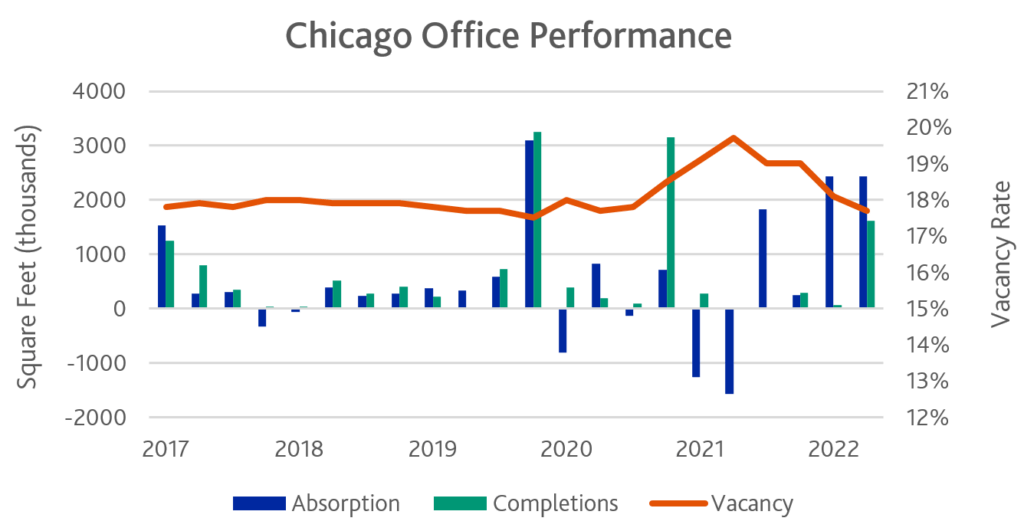

Q2 2021 thru Q2 2022

Inventory: +2,700,859 sq ft

Total Vacant: +1,808,274 sq ft

Direct Vacant: +2,177,696 sq ft

Sublet Vacant: -369,422 sq ft

Q3 2021

Net Inventory: +113658

Net Vacant: +1,749,800

Direct Vacant: +1,484,985

Sublet Vacant: +264,815

Q4 2021

Net Inventory: +388,356

Net Vacant: -571,715

Direct Vacant: +195,265

Sublet Vacant: -766,980

Q1 2022

Net Inventory: +2,151,055

Net Vacant: +130,485

Direct Vacant: +384,659

Sublet Vacant: -254,174

Q2 2022

Net Inventory: +47,790

Net Vacant: +499,804

Direct Vacant: +112,887

Sublet Vacant: +386,917

Prev

Prev

Linear Mode

Linear Mode