Posted Oct 11, 2014, 6:00 PM

Posted Oct 11, 2014, 6:00 PM

|

|

Registered User

|

|

Join Date: Aug 2002

Location: Toronto

Posts: 52,200

|

|

|

Is Wall Street Making a Killing off Cities’ Debt?

Is Wall Street Making a Killing off Cities’ Debt?

Oct 6, 2014

By Susie Cagle

Read More: http://nextcity.org/forefront/view/p...on-cities-debt

Quote:

.....

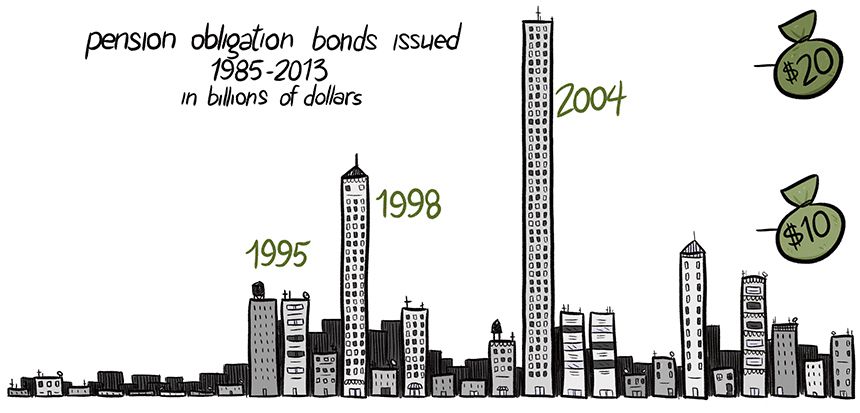

Since Oakland took out the first market-based bet on its pension fund nearly 30 years ago, municipal agencies across the country have used pension obligation bonds time and again to meet their bottom lines.

- Municipal bonds used to be a city’s way of funding a big infrastructure project that would otherwise be beyond the reach of a general fund — almost everyone has needed a loan now and then. But as tax revenue fell and expenses rose, cities increasingly borrowed against payments they’d contractually promised to their own workers. When those deals didn’t pan out, some cities made even bigger bets, swapping their debts for variable interest rates offered by large financial institutions.

- Many were losing bets. A handful of cities and counties went bankrupt balancing the debt on top of myriad other financial obligations. Others are stuck with huge interest payments on top of their unpaid principles. Meanwhile banks continue to rake in the profits at the expense of taxpayers, despite federal inquiries and settlements. --- Thanks mostly to a newly recovering market, American cities are limping back toward solvency, and the municipal bond market is making a comeback. But rebound aside, urban America remains sorely dependent on Wall Street and continues to pay dearly for the relationship — and it’s not clear how broke municipalities can get out of the bind.

- As local purse strings constrict ever tighter, cities have leaned even more heavily on debts to keep things running. Pension obligation bonds have proven to be one of the more popular lines of city credit. The premise of these bonds is that cities are able to postpone contributing to pension funds by borrowing from banks at a lower rate of interest than those invested funds will earn over the long term. As of 2009, Oregon, Illinois and Connecticut each have taken on more than 10 percent of their annual revenue on pension bonds.

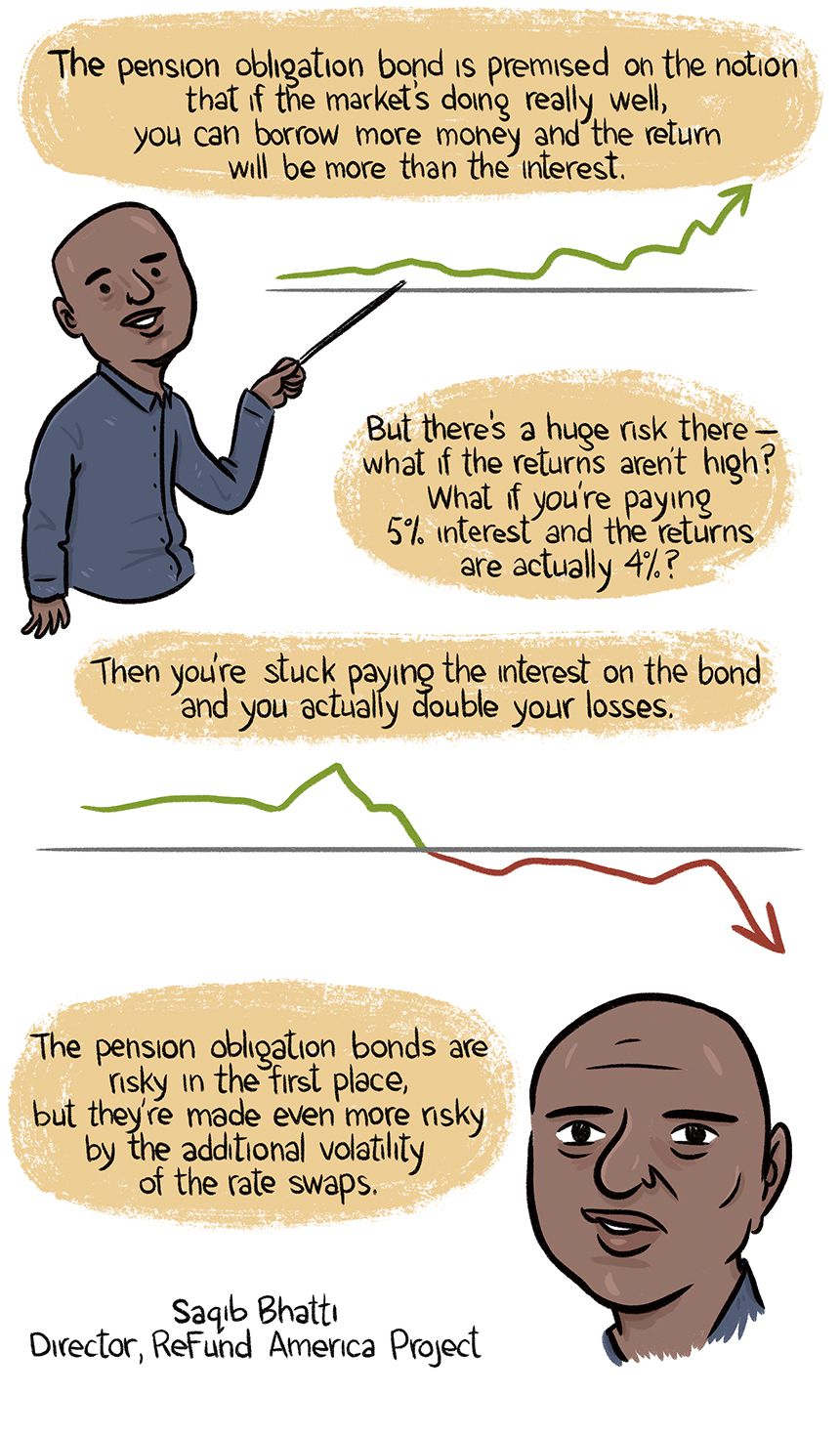

- When cities found their bottom lines still wanting, some gambled on interest rate swaps in an attempt to make up even more of the difference even more quickly. Essentially, they bet that the market where they’d invested their pension funds would continue to perform well, keeping interest rates high, so they traded their variable interest rates for fixed rates offered in new contracts by financial institutions that promised low risk and high savings.

- The market crashed, and so did those invested pension funds. “So all the times that instead of putting the money toward the pension you put it somewhere else — now there was a huge shortfall,” says Bhatti. Interest rate swaps only added insult to injury as the Fed lowered interest rates drastically while cities were still locked in to their old high interest rates on their bad bets with the banks. --- You couldn’t get out of one of these swaps unless you paid out all of the bank’s future potential earnings in one fell swoop.

- Oakland provides a solid example of just how critical timing is. In 2012, the city treasurer concluded that the swap had yielded a net benefit of $37.5 million in present-value savings from the swap. Earnings would have likely continued to outpace losses if the market hadn’t crashed in 2007. Furthermore, the consultant hired by the city treasurer to assess the swap did not find any evidence that Goldman had overcharged taxpayers. The unforeseen financial crisis and an overabundance of trust in the market was to blame.

- In 2005, Stockton, California was riding high, approving public projects left and right, enjoying the boosted property tax revenue of a bubbling housing market. Only two years later, it was on the verge of collapse. The subprime mortgage crisis had gutted the city and it was leading the nation in foreclosures. The stream of tax revenue the city had gotten used to dried up almost overnight. It was a fiscal drought the city hadn’t planned for and quickly the coffers emptied. In short order, Stockton owed $152 million to the state pension fund.

- In 2006, a Lehman Brothers representative came to town with an enticing offer: Make up that pension shortfall with $152 million in fixed-rate bonds. City officials weren’t sure they quite understood how the whole arrangement would work but they were desperate to keep parks open, police cars running and garbage men working; Lehman was offering a solution, even if nothing could be “guaranteed.” --- The bet didn’t work and Stockton never made up that pension shortfall. In 2012, the city filed for bankruptcy.

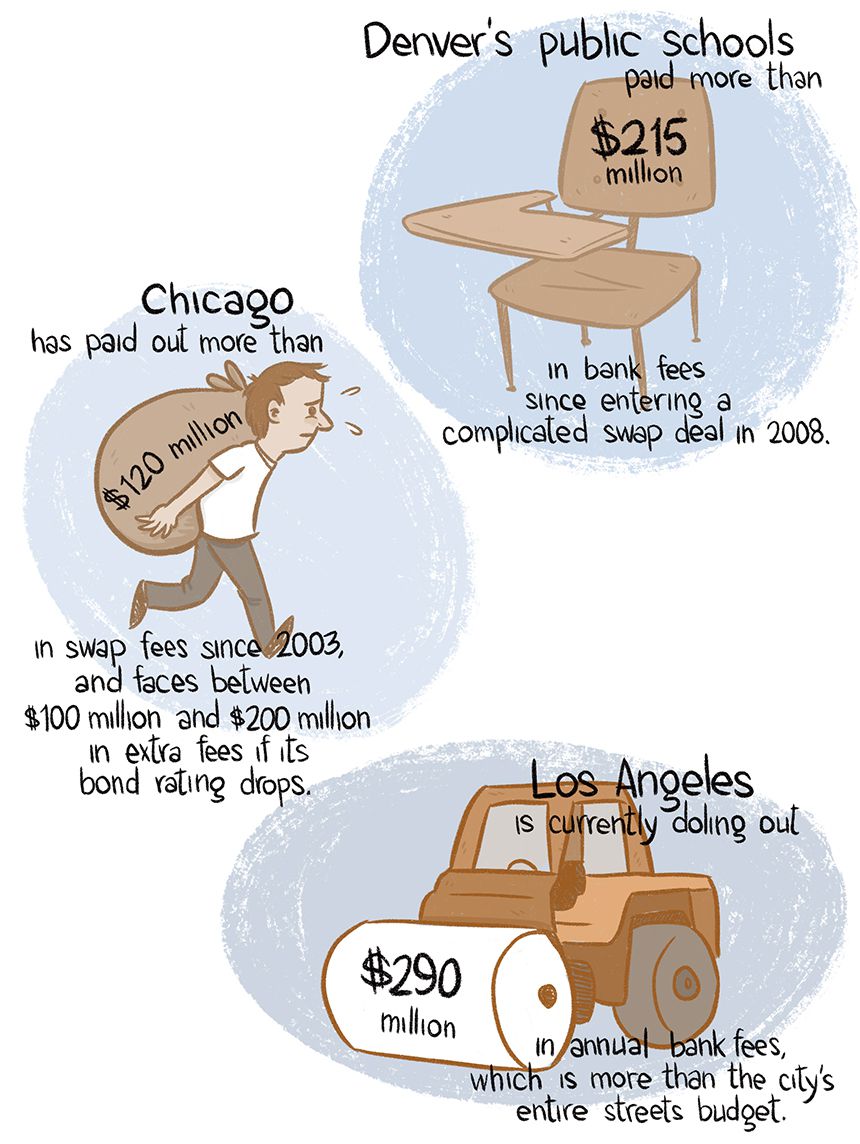

- Detroit’s collapse was not as sudden as Stockton’s — that once-great capital of American manufacturing had been in decline for decades. As the city shrank and its industry contracted, so too did its share of property and income tax revenues. Struggling to stay afloat as the state of Michigan also cut funds to the city, in 2005 and 2006, Detroit did as many others have done: it took out bonds in order to stay alive and avoid bankruptcy. Further, the city took out $800 million of those bonds on fixed rates that cost the city untold extra millions in inflated interest. --- As Detroit inched toward bankruptcy, its bond rating dropped, triggering a clause common in interest rate swap deals, and giving Wall Street an opening to collect all its once and future fees. Ultimately the banks were paid less than they wanted. But the hit they took is dwarfed by the sacrifices made by Detroit taxpayers and its pensioners.

- Oakland is not Stockton, nor is it Detroit. By many accounts, the city is now on the rise — Oakland’s proximity to Silicon Valley’s booming tech industry has boosted its business and real estate markets, in turn filling city coffers with new tax revenue, its first surplus in years. By many accounts, it’s a “renaissance” for a city long-troubled by unemployment, crime and debt. --- But the growth isn’t yet enough to push the city out of its fiscal hole. Oakland still faces $1.5 billion in long-term pension liabilities that it has promised to have under control by 2026. Some call it a “fiscal time bomb,” even with the city’s newly boosted income.

- Not only did banks sell cities on these bad deals without fully describing the risks — a possible crime in itself — but some financial institutions also conspired to be sure they were bad, colluding in order to make it seem as though cities received multiple competitive bids when in fact they only really received one, inflating the lending institution’s rate of return even further.

.....

|

__________________

ASDFGHJK

|

Linear Mode

Linear Mode